Table of Contents

- The Foreclosure Timeline for Homeowners: Stage by Stage

- Judicial vs Non-Judicial Foreclosure: How State Laws Shape Your Timeline

- Options for Homeowners Facing Foreclosure at Every Stage

- How to Stop Foreclosure Before the Auction Date

- Financial Documents Checklist: What to Gather Right Now

- What the Foreclosure Timeline Means for Your Credit and Future

- Avoiding Foreclosure Rescue Scams and Bad Advice

- Conclusion

Last Updated: June 8, 2026

The foreclosure timeline for homeowners is one of the most misunderstood processes in real estate law, and that misunderstanding costs people their homes every year. At My Foreclosure Options, we work with homeowners who discover too late that they had more time, more options, and more rights than anyone told them. This guide breaks down every stage of the foreclosure process, from the first missed payment to the eviction notice, so you know exactly where you stand and what you can do about it.

Most people assume foreclosure happens fast. It doesn’t. The legal process typically spans several months to well over a year depending on your state. The CFPB’s 120-day rule gives homeowners a significant window to act. The problem isn’t the timeline, it’s that homeowners don’t know it exists.

The Foreclosure Timeline for Homeowners: Stage by Stage

The foreclosure timeline follows a predictable legal sequence, but pace and procedures vary significantly by state. Understanding the structure lets you act strategically rather than reactively.

Stage 1: Mortgage Default and the 120-Day Rule

Mortgage default begins the moment you miss a payment. Most servicers will not initiate formal foreclosure until you are at least 120 days delinquent, a federal requirement under rules established by the Consumer Financial Protection Bureau mortgage servicing guidelines. During this window, your servicer is legally required to provide information about alternatives and assign you a single point of contact. Use this time. Do not wait for the servicer to call you.

A common mistake is ignoring servicer correspondence. Every letter, payment history summaries, inspection notices, loss mitigation deadlines, is legally significant.

Stage 2: Breach Letter and Notice of Intent to Foreclose

After a period of delinquency, your servicer will send a breach letter specifying the amount required to reinstate the loan and a deadline, typically 30 days. This is not yet a foreclosure filing, it is a legal prerequisite for one. Many homeowners either panic unnecessarily or ignore it entirely.

The right to cure your default before the deadline is one of your most important legal protections. If you can reinstate, do it. If you cannot, this is the point where contacting a HUD-approved housing counselor becomes critical.

Stage 3: Foreclosure Filing and Summons and Complaint

Once the breach letter deadline passes, the lender can file a formal foreclosure. In judicial states, this means a summons and complaint in court. In non-judicial states, the process moves through a trustee. If you receive a summons and complaint, respond. Failing to do so results in a default judgment that accelerates the timeline considerably. From this point forward, save and date every document and every communication with your servicer.

Stage 4: Foreclosure Sale and Auction

Once a sale date is set, the clock runs fast. The property is auctioned, and the highest bidder takes title. If the property sells for less than the outstanding balance, the lender may pursue a deficiency judgment for the remainder, depending on your state’s laws. Know your state’s rules before the sale date arrives.

Stage 5: Redemption Period and Eviction Process

Some states grant a redemption period after the sale during which the former homeowner can reclaim the property by paying the full sale price plus costs. Periods vary widely, from a few days to over a year. If no redemption occurs, the new owner initiates a separate eviction proceeding that requires proper legal notice before you can be removed. Understanding this distinction prevents homeowners from leaving too early and losing weeks of additional time to arrange housing.

Judicial vs Non-Judicial Foreclosure: How State Laws Shape Your Timeline

State law is the single biggest variable in the foreclosure timeline. Two homeowners with identical loan situations can face timelines differing by 12 months or more based solely on their state.

Judicial Foreclosure States: What to Expect

Judicial foreclosure requires the lender to file a lawsuit and obtain a court order before selling the property. The process creates multiple intervention points where a homeowner can raise defenses, request mediation, or negotiate alternatives. States like New York, New Jersey, Florida, and Illinois use judicial foreclosure. The disadvantage: missing court deadlines can collapse your timeline faster than the non-judicial process would.

Non-Judicial Foreclosure States: A Faster Process

Non-judicial foreclosure operates through a deed of trust and trustee, bypassing the courts entirely. The lender issues a notice of default, waits the required statutory period, then schedules a trustee’s sale, often completing in three to six months. States like California, Texas, Arizona, and Georgia primarily use this process. Homeowners in these states must act on loss mitigation options earlier, often before the formal notice of default is issued.

According to HUD’s state-by-state foreclosure process overview, procedures, notice periods, and redemption rights differ significantly across all 50 states. Knowing your state’s process is the foundation of any effective response strategy.

If you are unsure whether your state uses judicial or non-judicial foreclosure, your county recorder’s office or a HUD-approved housing counselor can tell you immediately. This single piece of information shapes every other decision you make.

Options for Homeowners Facing Foreclosure at Every Stage

Options do not disappear once the process begins. Many homeowners assume that once they receive a notice of default, their choices are gone. This is wrong, and it is one of the most damaging misconceptions in the entire foreclosure process.

Forbearance, Loan Modification, and Reinstatement

Forbearance is a temporary pause or reduction in payments granted by the servicer. It does not eliminate what you owe, missed payments must eventually be repaid as a lump sum, repayment plan, or addition to the loan term.

Loan modification permanently changes your mortgage terms, interest rate, loan term, or loan type, and requires a formal application with financial documentation.

Reinstatement is the simplest option: pay everything owed, including missed payments, late fees, and servicer costs, in one lump sum before the sale date. If you have access to funds, reinstatement stops foreclosure immediately and returns your loan to current status.

Short Sale, Deed in Lieu, and Foreclosure Mediation

A short sale lets you sell the property for less than the outstanding balance with lender approval, accepting the proceeds as full or partial satisfaction of the debt. Initiate early, lender approval takes time.

A deed in lieu of foreclosure transfers ownership directly to the lender in exchange for release from the mortgage obligation. Lenders generally require that you attempt a short sale first.

Foreclosure mediation, available in many judicial states, uses a neutral mediator to facilitate negotiation between homeowner and lender. Requests must typically be filed within a specific window after receiving the summons and complaint. Mediation doesn’t guarantee resolution, but it creates a structured environment for reaching one.

How to Stop Foreclosure Before the Auction Date

Stopping foreclosure before the auction date is achievable at nearly every stage, but available tools narrow as the sale date approaches.

The most direct path is selling the property before the auction. If you have equity, a conventional sale gives you the most control. If equity is limited or time is short, a cash buyer can close in days. This stops the foreclosure, eliminates the mortgage debt, and preserves whatever equity remains. My Foreclosure Options connects homeowners with vetted cash buyers nationwide and can structure a sale timeline around your specific situation.

Bankruptcy is another tool, though with significant long-term consequences. Filing Chapter 13 triggers an automatic stay that halts foreclosure immediately and buys time to propose a repayment plan. It requires legal counsel to execute properly.

Do not file for bankruptcy without consulting a bankruptcy attorney first. Improper filings can be dismissed quickly, leaving you with fewer options and less time than before you filed.

Contacting your servicer directly to request a loss mitigation review is always worth doing, even close to the sale date. Servicers are generally prohibited from dual-tracking, they cannot proceed with a foreclosure sale while a complete loss mitigation application is under review. Submit in writing, keep copies, and document every communication.

Financial Documents Checklist: What to Gather Right Now

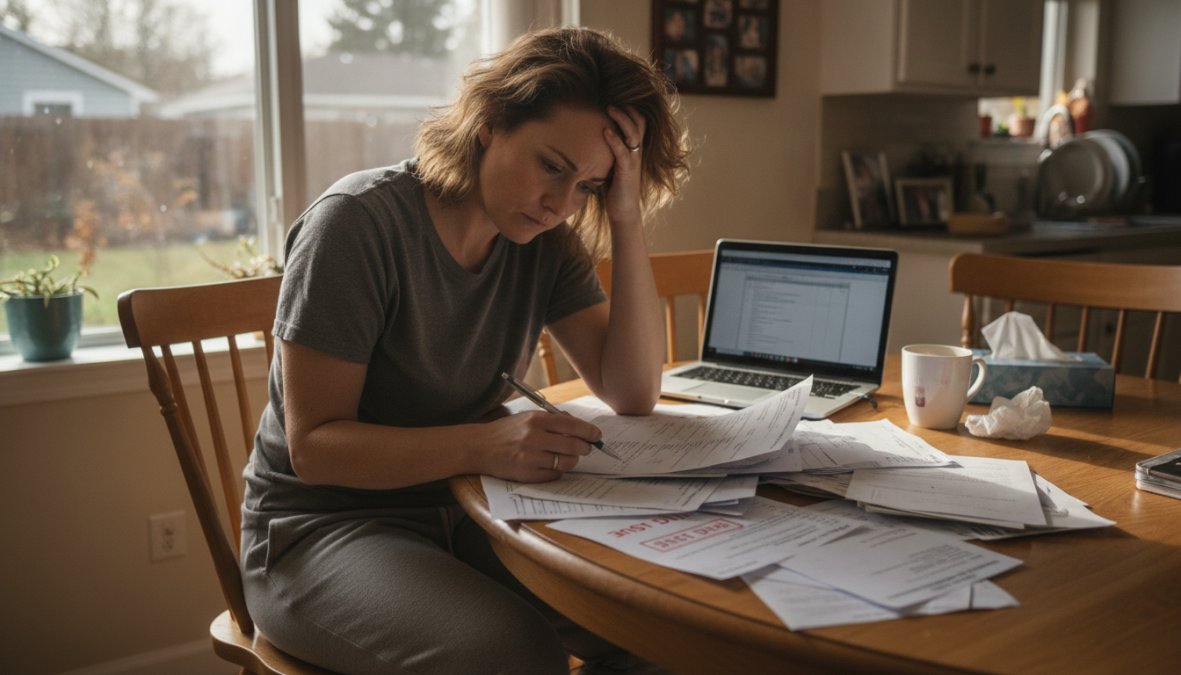

Gathering your financial documents before contacting your servicer, a housing counselor, or an attorney dramatically speeds up the loss mitigation process. Incomplete applications are one of the most common reasons homeowners lose their window.

Gather these documents immediately:

- Last two years of federal tax returns

- Last two months of bank statements for all accounts

- Last two months of pay stubs or proof of income

- Most recent mortgage statement showing current balance and payment history

- Proof of any other income: rental income, Social Security, disability, alimony

- A written hardship letter explaining the circumstances that led to delinquency

- Most recent property tax statement

- Homeowner’s insurance declarations page

- Any correspondence received from your servicer, including all notices and letters

- HOA statements if applicable

According to CFPB guidance on loss mitigation applications, servicers must acknowledge receipt of a complete application within five business days and provide a decision within 30 days if received more than 37 days before a scheduled sale.

A complete loss mitigation application, submitted in writing with all supporting documents, is your single most effective tool for stopping a foreclosure sale. Incomplete applications are the primary reason applications are denied or delayed.

What the Foreclosure Timeline Means for Your Credit and Future

The foreclosure timeline for homeowners does not end at the auction. The financial consequences extend well beyond the loss of the property, but they are not permanent.

Post-Foreclosure Credit Recovery Roadmap

A completed foreclosure typically remains on your credit report for seven years from the date of the first missed payment. The impact diminishes over time with consistent positive credit behavior. A practical recovery sequence:

- Year 1: Obtain your credit reports from all three bureaus and dispute inaccurate entries. Open a secured credit card and pay it in full monthly.

- Year 2: Add a credit-builder loan from a credit union to diversify your credit mix. Keep balances below 30% of available credit.

- Years 3-4: FHA loans require a three-year waiting period after foreclosure; many conventional programs require three to four years. Use this time to build savings and maintain a clean payment history.

- Years 5-7: With consistent credit management, many homeowners are mortgage-eligible again before the foreclosure drops off their report entirely.

The Psychological Impact and Where to Find Support

The psychological weight of foreclosure is real and often underestimated. Anxiety, shame, and decision paralysis are common, and they directly interfere with taking the practical steps that could change the outcome.

The most dangerous response is avoidance: homeowners stop opening mail, stop answering servicer calls, and lose weeks of critical response time. The foreclosure timeline does not pause for emotional recovery. If you are struggling, the SAMHSA National Helpline for mental health and financial stress provides free, confidential support. HUD-approved housing counselors are also trained to work with homeowners in crisis and can help you separate the emotional weight from the practical decisions.

Avoiding Foreclosure Rescue Scams and Bad Advice

The foreclosure rescue scam industry is predatory and specifically designed to target overwhelmed homeowners. Knowing the warning signs is a survival skill.

The most common patterns: a company promises to stop your foreclosure for an upfront fee, then disappears. Another asks you to sign over your deed "temporarily" while they work on your loan, then sells the property. A third instructs you to stop communicating with your servicer and pay them instead, while foreclosure proceeds uninterrupted.

Warning signs to watch for:

- Any company that guarantees to stop foreclosure for an upfront fee

- Requests to sign documents not reviewed by independent legal counsel

- Instructions to stop communicating with your mortgage servicer

- Offers to take over your mortgage payments directly

- Pressure to act immediately without time to review agreements

The FTC’s guidance on mortgage relief scams documents the most common fraud patterns. Legitimate HUD-approved housing counselors provide services free of charge or at low cost and never ask for deed transfers or upfront fees. The difference between a legitimate advisor and a scam is transparency: legitimate advisors explain exactly what they are doing, put everything in writing, and never ask you to hand over control of your property.

Facing foreclosure is one of the most stressful financial situations a homeowner can experience. My Foreclosure Options provides confidential, no-pressure guidance to help you understand your position, explore every available option, and connect with cash buyers who can close quickly and stop the auction before it happens. Founded by retired U.S. Navy veteran Chad Overly, with 22 years of service, the team brings a direct, honest approach to protecting your equity and credit. Check My Options today and get a clear picture of what’s available to you before time runs out.

Frequently Asked Questions

How long does the foreclosure process take from start to finish?

The foreclosure timeline for homeowners varies widely by state and foreclosure type. In judicial foreclosure states, the process can take anywhere from 6 months to over 2 years due to court involvement. Non-judicial foreclosure states can move much faster, sometimes completing the process in 3 to 6 months. Federal rules also require loan servicers to wait at least 120 days after a missed payment before initiating foreclosure, giving homeowners a window to explore loss mitigation options.

How many missed payments before foreclosure begins?

Under CFPB rules, a loan servicer generally cannot begin the formal foreclosure process until a homeowner is more than 120 days delinquent. This is often referred to as the 120-day rule. However, after just one missed payment, your servicer may begin contacting you. After 90 days of delinquency, you will typically receive a breach letter or notice of default. Acting early, even after the first missed payment, gives you the most options to stop foreclosure.

Can you stop a foreclosure once it has started?

Yes, homeowners facing foreclosure have several options to stop or delay the process even after it has begun. These include requesting a loan modification, entering a forbearance agreement, pursuing a short sale, filing a mediation request, or selling the property before the auction date. Working with a HUD-approved housing counselor or contacting the HOPE hotline can help you identify which option fits your situation. Acting quickly is critical, options narrow significantly as the foreclosure sale date approaches.

What is the difference between judicial and non-judicial foreclosure for homeowners?

Judicial foreclosure requires the loan servicer to file a lawsuit and obtain a court order before selling the property. This process involves a summons and complaint, and potentially a default judgment if the homeowner does not respond. Non-judicial foreclosure, also called a power of sale process, does not require court involvement and follows a timeline set by state law. Judicial states generally offer homeowners more time and procedural protections, while non-judicial states move faster with less opportunity to contest the process.

What happens after a notice of default is filed?

After a notice of default is filed, homeowners typically enter a right-to-cure period during which they can bring the loan current through reinstatement, paying all overdue amounts, fees, and costs. If the delinquency is not cured, the loan servicer proceeds toward a foreclosure sale. Homeowners should immediately contact their servicer's single point of contact, consult a housing counselor, and explore loss mitigation options such as loan modification, forbearance, or a short sale to prevent the property from going to auction.

Does the foreclosure timeline vary by state?

Yes, the foreclosure timeline for homeowners differs significantly by state. States like New York and New Jersey have lengthy judicial processes that can extend the timeline well beyond a year. States like Texas, Georgia, and California use non-judicial processes that can conclude in as few as 90 to 120 days after the notice of default. Some states also provide a post-sale redemption period, allowing homeowners to reclaim their property after the foreclosure auction by paying the full sale amount. Knowing your state's rules is essential to protecting your rights.

This article was written using GrandRanker