Table of Contents

- How to Stop the Foreclosure Process Before It’s Too Late

- Foreclosure Timeline by State: Know Your Deadlines

- The Loan Modification Application Process Explained

- How to File for Chapter 13 Bankruptcy to Stop Foreclosure

- Deed in Lieu of Foreclosure: Pros and Cons You Must Know

- Working With a HUD-Approved Housing Counselor and Avoiding Scams

- Selling Your Home to Stop Foreclosure and Protect Your Equity

- Post-Foreclosure Recovery: Rebuilding Your Credit and Future

Last Updated: June 4, 2026

How to Stop the Foreclosure Process Before It’s Too Late

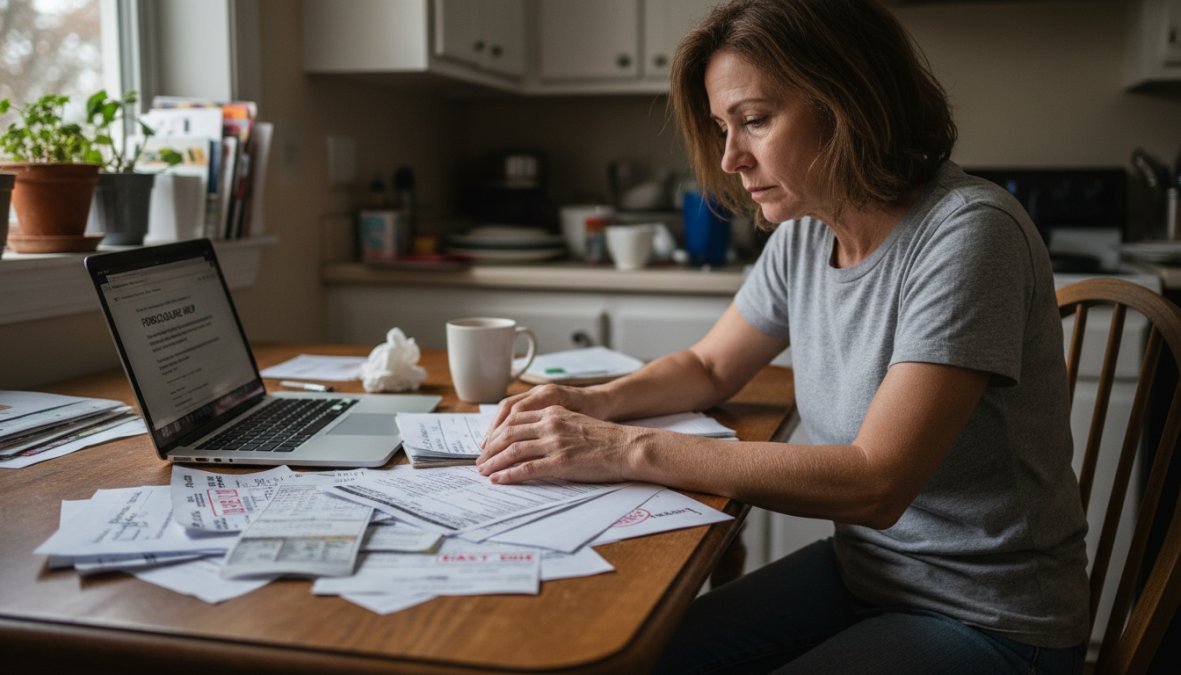

Foreclosure is not inevitable, even after several missed payments. Knowing how to stop foreclosure process actions before they escalate can mean the difference between keeping your home and losing it at auction. This guide covers every realistic option available to homeowners in 2026, from contacting your mortgage servicer on day one to understanding bankruptcy protections and selling on your own terms. Strategies are arranged by urgency so you can act fast regardless of where you are in the timeline.

What most guides get wrong: they treat foreclosure as a legal inevitability rather than a negotiation. Lenders generally prefer loss mitigation over the cost and delay of foreclosure proceedings, which gives homeowners more leverage than they realize.

Understanding Default and Delinquency: Where You Stand

Delinquency begins after a single missed payment. Default is the formal legal status that triggers foreclosure, usually after 90 to 120 days of missed payments depending on your loan terms and state law.

Your options narrow as time passes. Early delinquency gives you the widest range: repayment plans, forbearance, and loan modification are all available. Once your lender records a Notice of Default, the clock accelerates and documentation requirements become more demanding. A common mistake is waiting for the lender to reach out first, by the time they do, you may have already missed the window for the easiest solutions.

Your First Call: Contacting Your Mortgage Servicer

Call your mortgage servicer the moment you anticipate missing a payment. Ask specifically for the loss mitigation department. Have ready: your loan account number, a brief explanation of your hardship, and recent income documentation. Under CFPB regulations, servicers must acknowledge a complete loss mitigation application within five business days and provide a decision within 30 days.

Request the name and direct extension of every representative you speak with. Document the date, time, and summary of every call. This paper trail protects you if the servicer later claims they never received your application.

Foreclosure Timeline by State: Know Your Deadlines

State law governs how quickly a lender can move from default to foreclosure sale. Some states allow completion in as few as 60 days; others provide more than a year. According to CFPB housing resources and foreclosure timelines, understanding your state’s specific timeline is one of the first steps any homeowner in default should take.

| State Type | Typical Timeline | Key Feature |

|---|---|---|

| Fast non-judicial states | 60-120 days | No court involvement required |

| Average judicial states | 6-18 months | Court must approve each step |

| Slow judicial states | 18-36 months | Extended redemption periods |

| States with right of redemption | Varies | Homeowner can reclaim after sale |

Acting early is always better, but if you’re in a judicial foreclosure state you have more time to pursue loan modification or a short sale before auction.

Judicial vs. Non-Judicial Foreclosure States

Judicial foreclosure requires the lender to file a lawsuit and obtain a court order before selling the property. Homeowners receive formal notice and can respond legally. States like Florida, New York, and Illinois use this process.

Non-judicial foreclosure follows a statutory process outside the courts using a "power of sale" clause. Lenders in states like California, Texas, and Georgia can move significantly faster, making early action critical. Wrongful foreclosure claims are also easier to pursue in judicial states because the court record documents every procedural step.

The Loan Modification Application Process Explained

A loan modification permanently changes one or more terms of your original mortgage, interest rate, loan term, or principal balance, to reduce your monthly payment. It is the most common path homeowners use to stop foreclosure and restructure debt. The process typically takes 30 to 90 days from application to approval, though complex cases run longer.

Never stop making payments because you’ve submitted a modification application. Servicers can still advance foreclosure proceedings during a review unless you receive written confirmation of a foreclosure hold. Stopping payments without that confirmation accelerates your delinquency.

Step-by-Step Documentation Checklist for Loss Mitigation

A complete, well-organized loss mitigation package significantly increases approval odds. Missing even one document causes delays that can cost you weeks.

Loss Mitigation Documentation Checklist:

- Completed borrower assistance form (provided by your servicer)

- Hardship letter explaining the cause and current status of your financial hardship

- Two most recent federal tax returns

- Two most recent pay stubs for all employed borrowers

- Most recent bank statements (all accounts, all pages, last 2-3 months)

- Profit and loss statement if self-employed (last 12 months)

- Documentation of any other income: Social Security, disability, rental income

- Most recent mortgage statement

- HOA assessment statements if applicable

- Proof of property taxes paid or delinquent (county tax bill)

Submit everything at once via certified mail or the servicer’s secure online portal. Keep copies of every document and follow up in writing every 10 days until you receive written acknowledgment.

How to File for Chapter 13 Bankruptcy to Stop Foreclosure

Chapter 13 bankruptcy is one of the most effective legal tools for homeowners facing imminent foreclosure. The moment you file, an automatic stay legally prohibits your lender from taking any further foreclosure action while the case is active. Chapter 13 is a reorganization bankruptcy: you propose a 3-to-5-year repayment plan that catches up on mortgage arrears while continuing current payments. As documented in U.S. Courts official bankruptcy information, Chapter 13 specifically protects homeowners’ primary residences in ways Chapter 7 cannot.

Chapter 7 vs. Chapter 13: Which Option Fits Your Situation

The choice comes down to one question: do you have regular income and a genuine desire to keep the home?

Chapter 13 is right if you have steady income, want to keep your home, and can afford current mortgage payments going forward. It allows you to repay arrears over the plan while stopping foreclosure immediately.

Chapter 7 is a liquidation bankruptcy. The automatic stay temporarily stops a foreclosure sale, but once Chapter 7 concludes the lender can resume proceedings. It is better suited to homeowners who want to discharge unsecured debt and exit the property without a deficiency judgment.

| Factor | Chapter 13 | Chapter 7 |

|---|---|---|

| Stops foreclosure long-term | Yes | Temporarily only |

| Requires regular income | Yes | No |

| Keeps your home | Possible | Unlikely |

| Duration | 3-5 years | 3-6 months |

| Discharges unsecured debt | Partially | Fully |

Consult a bankruptcy attorney before filing either type. Legal assistance is worth the investment when your home is at stake.

Deed in Lieu of Foreclosure: Pros and Cons You Must Know

A deed in lieu of foreclosure is an agreement where you voluntarily transfer ownership to the lender in exchange for release from your mortgage obligation.

Pros:

- Avoids the public record of a formal foreclosure sale

- Typically faster and less damaging to credit than a completed foreclosure

- May include a "cash for keys" agreement from the lender

- Eliminates ongoing property tax and HOA obligations immediately upon transfer

Cons:

- Lenders frequently decline if there are junior liens on the property

- You lose all home equity, even if property value exceeds the loan balance

- Forgiven debt may be treated as taxable income in some circumstances

- Credit impact is still significant, though generally less severe than a foreclosure judgment

The deed in lieu of foreclosure pros and cons calculation shifts with your equity position. If you have substantial equity, selling outright is almost always better. A deed in lieu only makes financial sense when the property is worth less than the outstanding mortgage balance and no other options remain.

A deed in lieu of foreclosure is a last resort for underwater properties, not a first option. Homeowners with equity should explore a traditional or quick sale before agreeing to transfer the deed.

Working With a HUD-Approved Housing Counselor and Avoiding Scams

Free expert help is available through HUD-approved housing counselors, certified professionals who can review your mortgage documents, explain your rights, prepare a loss mitigation application, and communicate with your servicer on your behalf. Their services are free.

According to HUD’s official housing counselor locator, you can find a HUD-approved counselor by calling 1-800-569-4287 or using the agency’s online search tool. This is the single most underused resource in foreclosure prevention.

How to Spot and Avoid Foreclosure Rescue Scams

Foreclosure rescue scams follow predictable patterns. Knowing them protects you.

Red flags that signal a scam:

- Upfront fees before any service is delivered. Legitimate HUD-approved counselors never charge upfront fees.

- Guarantees of loan modification approval. No third party can guarantee a lender’s decision.

- Requests to sign over your deed. Scammers promise to "save" your home by taking title, then collect rent while you lose ownership.

- Instructions to stop communicating with your lender. Cutting off lender communication accelerates foreclosure.

- High-pressure timelines. Scammers create artificial urgency to prevent you from seeking a second opinion.

Verify any company through the CFPB consumer complaint database before signing anything.

Selling Your Home to Stop Foreclosure and Protect Your Equity

Selling before the foreclosure auction is the most effective way to protect your equity and credit when keeping the property is no longer realistic. A foreclosure sale typically produces a below-market price, and any equity disappears into the process. If your home is worth more than your outstanding mortgage balance plus selling costs, a voluntary sale puts money in your pocket.

For homeowners with limited time before a scheduled auction, a cash sale is often the fastest path, cash buyers can close in days rather than weeks. My Foreclosure Options connects homeowners with vetted cash buyers nationwide, offering a confidential, no-pressure review of your situation structured to protect your equity and accommodate your move timeline.

A short sale, where the lender agrees to accept less than the full mortgage balance from a third-party buyer, is another option when the property is underwater. Short sales require lender approval and take longer, but typically produce better credit outcomes than a completed foreclosure.

Managing the Mental Health and Stress of Facing Foreclosure

Foreclosure is not just a financial event. The stress of potential home loss affects sleep, relationships, decision-making, and physical health, and often causes homeowners to delay action, making every available option worse.

The shame associated with financial hardship causes many people to avoid calls from servicers and counselors, accelerating the very outcome they fear. Reaching out for help is the most strategically sound move available. If stress is affecting your ability to function, contact the SAMHSA National Helpline for mental health support or a local financial counseling nonprofit. Many HUD-approved agencies also provide mental health referrals alongside housing counseling. Taking care of your mental state is a prerequisite for solving the foreclosure problem clearly.

Post-Foreclosure Recovery: Rebuilding Your Credit and Future

A completed foreclosure stays on your credit report for seven years, but its impact diminishes significantly after two to three years of consistent positive credit behavior. Recovery is real and achievable.

The most important steps in the first 12 months after foreclosure:

- Obtain your credit reports from all three bureaus and dispute any inaccuracies in how the foreclosure is reported.

- Open a secured credit card and use it for small recurring purchases, paying the balance in full each month.

- Avoid new debt beyond what you can manage and pay on time.

- Build an emergency fund, even a small one, to prevent the next hardship from becoming a crisis.

- Track your credit score monthly using a free monitoring service to measure progress.

FHA-insured loan programs allow homeowners to apply for a new mortgage as soon as three years after foreclosure. Conventional programs typically require four to seven years depending on circumstances, with shorter waiting periods if you can document an extenuating circumstance beyond your control.

The foreclosure process feels permanent when you’re inside it. It isn’t. Homeowners who take early action and make clear-eyed decisions consistently reach better outcomes than those who wait.

Facing foreclosure is one of the most stressful situations a homeowner can experience, and the window for effective action closes faster than most people realize. My Foreclosure Options provides confidential, no-pressure guidance to homeowners nationwide, with fast connections to cash buyers who can help you sell before auction and protect your remaining equity. Founded by retired U.S. Navy veteran Chad Overly, the team brings 22 years of disciplined service to every homeowner consultation. Check My Options today to get a quick review of your specific situation and understand exactly what’s available to you.

Frequently Asked Questions

Can you stop a foreclosure once it has started?

Yes, you can stop the foreclosure process even after it has started. Options include contacting your mortgage servicer to request forbearance or a repayment plan, applying for a loan modification, filing for Chapter 13 bankruptcy to trigger an automatic stay, or selling your home before the foreclosure auction. Acting quickly is critical, the earlier you engage with your servicer or a HUD-approved housing counselor, the more options remain available to you.

Does filing for bankruptcy stop foreclosure immediately?

Filing for Chapter 13 bankruptcy triggers an automatic stay, which legally halts the foreclosure process immediately upon filing. This gives you time to restructure your mortgage debt through a court-approved repayment plan. Chapter 7 bankruptcy can also pause foreclosure temporarily, but it does not provide a long-term path to keeping your home. Consult a bankruptcy attorney to determine which option best fits your financial hardship situation.

How long does the foreclosure process take by state?

The foreclosure timeline by state varies significantly. Judicial foreclosure states like New York and Florida can take 12 to 36 months or longer because the lender must go through the court system. Non-judicial foreclosure states like California and Texas can move much faster, sometimes completing the process in 90 to 180 days. Knowing your state's timeline is essential, it determines how urgently you need to act to stop foreclosure before the auction date.

What is the loan modification application process?

The loan modification application process involves contacting your mortgage servicer and formally requesting loss mitigation assistance. You will need to submit a hardship letter, recent pay stubs or proof of income, bank statements, tax returns, and a completed financial worksheet. Your servicer reviews your application to determine if you qualify for a modified interest rate, extended loan term, or reduced payment. Working with a HUD-approved housing counselor can strengthen your application and help you avoid costly mistakes.

What are the pros and cons of a deed in lieu of foreclosure?

A deed in lieu of foreclosure lets you voluntarily transfer your home's title to the lender in exchange for canceling your mortgage debt, avoiding a formal foreclosure sale. Pros include avoiding a public foreclosure auction, potentially negotiating relocation assistance, and less severe credit damage than a full foreclosure. Cons include losing your home entirely, possible tax liability on forgiven debt, and the lender may still pursue a deficiency judgment in some states. It is not always accepted if there are secondary liens on the property.

Can I sell my house to stop foreclosure?

Yes, selling your home before the foreclosure auction is one of the fastest ways to stop the foreclosure process and protect your equity and credit. A traditional sale or a sale to a cash buyer can close quickly, allowing you to pay off the outstanding mortgage balance. If you owe more than the home is worth, a short sale, where the lender agrees to accept less than the full balance, may also be an option. Acting before the auction date preserves the most financial options.

This article was written using GrandRanker